February 19, 2026

Last Updated: January 2026

The AI search landscape has undergone its most dramatic transformation since ChatGPT's launch. ChatGPT's near-monopoly has fractured, Google Gemini has emerged as a formidable challenger, and specialized platforms like Perplexity and Claude have carved out significant niches.

This analysis breaks down the current market share data and what it means for your AI search strategy.

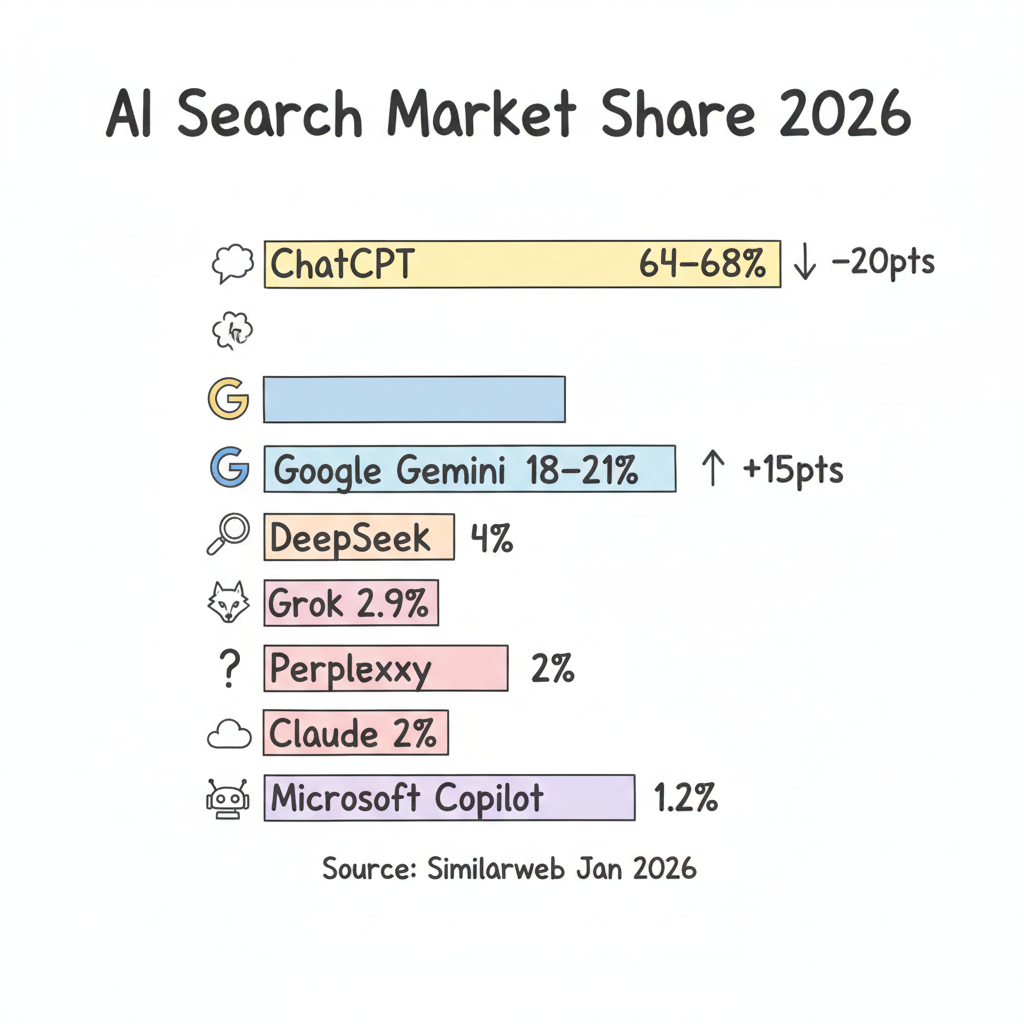

According to Similarweb data released in January 2026, the AI chatbot market has redistributed significantly:

Platform | Market Share (Jan 2026) | Market Share (Jan 2025) | YoY Change |

ChatGPT (OpenAI) | 64.5-68% | 86.7-87.2% | -19 to -22 pts |

Google Gemini | 18.2-21.5% | 5.4-5.7% | +13 to +16 pts |

DeepSeek | 4% | <1% | +3+ pts |

Grok (X.AI) | 2.9% | <1% | +2+ pts |

Perplexity | 2% | <1% | +1+ pts |

Claude (Anthropic) | 2% | <1% | +1+ pts |

Microsoft Copilot | 1.2% | ~1% | Stable |

ChatGPT's 19+ percentage point decline represents the most significant market shift in generative AI history—signaling the end of OpenAI's near-monopolistic position.

The raw user numbers tell a compelling story about scale:

Platform | Monthly Active Users |

Google Search | 5 billion |

ChatGPT | 800-858 million |

Google Gemini | 650 million |

Perplexity | 45 million |

Microsoft Copilot | 33 million |

Grok | 30 million |

Claude | 19 million |

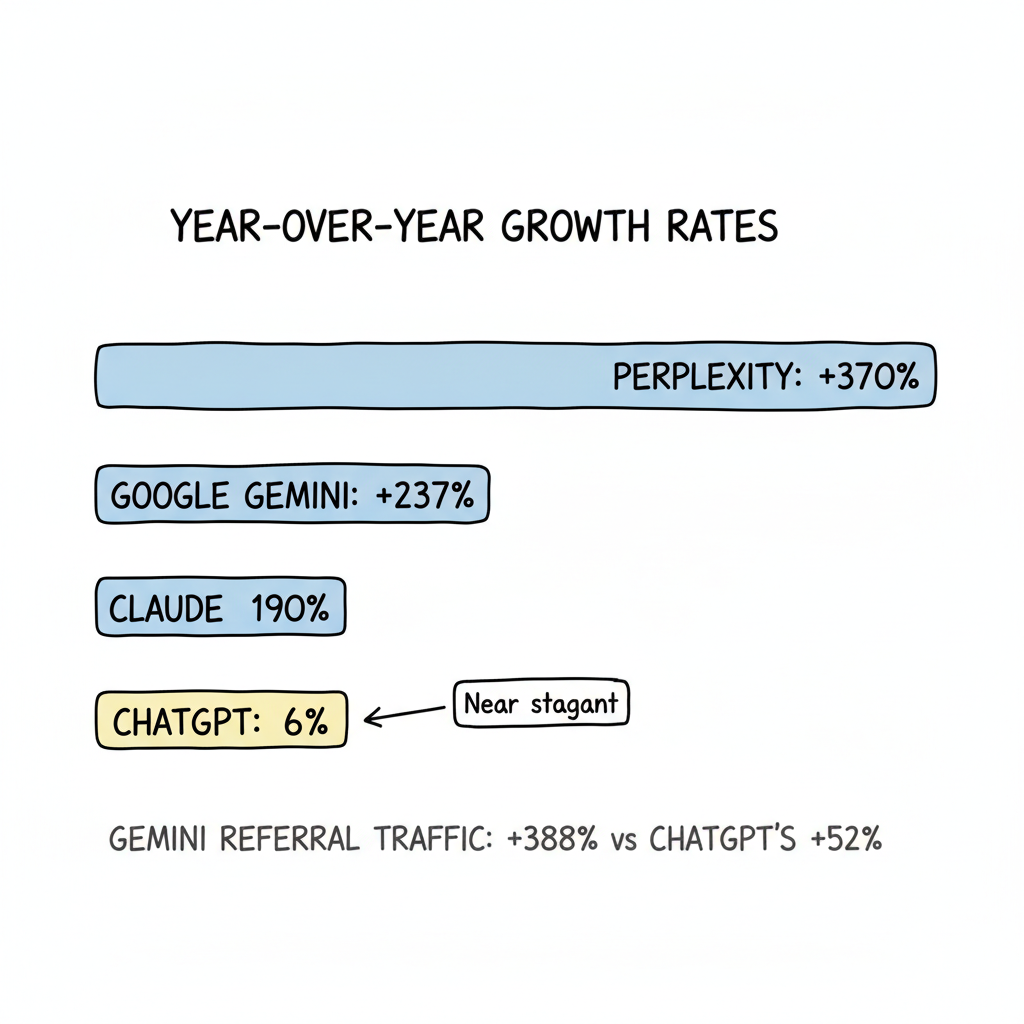

Year-over-year growth reveals which platforms are gaining momentum:

Gemini's referral traffic growth outpaces ChatGPT by more than 7x, making it an increasingly important web entry point.

Different platforms dominate different query types. Understanding what is an answer engine helps explain why these platforms excel at different intents:

Query Type | Google Share | ChatGPT Share |

Navigational | Higher | Lower |

Informational | Moderate | Higher |

Transactional | Higher | Growing |

Local | Dominant | Minimal |

ChatGPT shows particular strength in informational and creative queries, while Google maintains dominance in navigational and local search.

Age significantly influences platform preference:

Age Group | Google Share | ChatGPT Share |

13-24 | 74% | 17% |

25-44 | 80% | 13% |

45-64 | 86% | 8% |

65+ | 89% | 5% |

Younger users adopt AI-native platforms faster, while older demographics remain Google-centric.

Platform | Desktop Share | Mobile Share |

Google Search | 37% | 63% |

ChatGPT | 62% | 38% |

ChatGPT sees stronger desktop engagement (suggesting professional and research use), while Google dominates mobile usage among casual and on-the-go users.

Despite losing nearly 20 percentage points, ChatGPT isn't collapsing—it's stabilizing. Projections suggest ChatGPT will settle around 50-55% market share as it loses casual users but retains engaged power users.

Google's integration of Gemini directly into Search and Workspace generates millions of interactions per second. This distribution advantage creates a data flywheel that improves the model without additional training. The shift from Google AI Overview vs traditional SERP has fundamentally changed how users encounter AI-powered results.

Niche players are thriving by avoiding direct competition with giants:

Perplexity (370% growth): Positioned as an AI-first search engine rather than a general chatbot, targeting research and citation-heavy use cases.

Claude (190% growth): Focused on enterprise customers prioritizing responsible AI deployment, generating $2.2 billion in projected 2025 revenue.

Markets outside the US show different patterns:

The transition from chatbots to AI agents is resetting competitive dynamics. Platforms that can execute actions—not just answer questions—are gaining strategic advantage.

With no single platform dominating, optimizing for just one AI search engine means missing significant traffic. The fragmented market requires presence across multiple AI-powered search tools:

Each platform evaluates content differently. Developing a comprehensive AEO strategy means tailoring your approach to each platform's unique ranking factors:

The 17% of 13-24 year-olds using ChatGPT today represents future search behavior. Brands targeting younger demographics need AI visibility now.

ChatGPT's desktop dominance (62%) suggests professional usage patterns. Enterprise-focused businesses should prioritize ChatGPT and Claude visibility, while consumer brands need broader coverage including mobile-dominant Google.

Based on current trajectories:

Model capabilities are becoming commoditized. Differentiation is shifting toward integrations, user experience, and specialized capabilities rather than raw model quality.

The AI search market has fragmented permanently. ChatGPT's monopoly era is over, replaced by a competitive ecosystem where Google Gemini, Perplexity, Claude, and others each control meaningful market share.

For businesses optimizing for AI visibility, this fragmentation means more work—but also more opportunity. Brands that build visibility across multiple platforms gain competitive advantages that single-platform optimizers miss.

The winners in 2026 and beyond will be those treating AI search as a multi-platform discipline, not a single-channel tactic.

By submitting this form, you agree to our Privacy Policy and Terms & Conditions.